No one likes paying too much, especially for insurance. Seems like everyone is constantly shopping for the best rates.

Nothing wrong with that. I always tell folks when you pay more you don't get more, you simply paid too much.

But it is also possible to pay too little for insurance. When you do, more often than not it comes back to bite you.

More often than not consumers would be wise to pay a few dollars more and get a plan without so many "gotcha's".

#PayingTooMuchForInsurance

from InsureBlog https://ift.tt/2wTZIoZ

via

Monday, 20 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

"I was told this today...with an effective date of applications starting tomorrow. I have several folk 65+ who are trying to apply, and I have to say sorry, but I have more expensive options for you to look at.

Throughout the rapidly evolving pandemic, Mutual of Omaha has been continuously evaluating our underwriting and new business practices to support business continuity, deliver a consistently high level of service, and maintain our financial strength.

As a result, effective Thursday, April 16, 2020, we are implementing a temporary change. We will not be accepting LTC applications for individuals age 65 and older. All LTC cases not already approved or issued will be postponed and processed as an incomplete application.

We will continue to prequalify applicants 64 and younger. The prequalification will be good for 60 days. If the health of the client changes or the prequalification is past 60 days, you will need to prequalify the applicant again."

I then confirmed this with FoIB Randy G, who added:

"MOO, TransAmerica, NGL, and Thrivent are not accepting any applications for those over the age of 65.

They say temporarily….

Reason is that individuals over the age of 65 will require a home face to face interview.

The nurses who conduct those interviews don’t have sufficient PPEs to enter homes.

Anyway, that’s the story I got.

The companies will still accept applications for those 64 and under. However, there are restrictions to this as well."

Thanks, Herman and Randy!

Oh, my take?

I think it's bullcrap: have none of these carriers ever heard of Skype?

from InsureBlog https://ift.tt/34QHgdc

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

"I was told this today...with an effective date of applications starting tomorrow. I have several folk 65+ who are trying to apply, and I have to say sorry, but I have more expensive options for you to look at.

Throughout the rapidly evolving pandemic, Mutual of Omaha has been continuously evaluating our underwriting and new business practices to support business continuity, deliver a consistently high level of service, and maintain our financial strength.

As a result, effective Thursday, April 16, 2020, we are implementing a temporary change. We will not be accepting LTC applications for individuals age 65 and older. All LTC cases not already approved or issued will be postponed and processed as an incomplete application.

We will continue to prequalify applicants 64 and younger. The prequalification will be good for 60 days. If the health of the client changes or the prequalification is past 60 days, you will need to prequalify the applicant again."

Throughout the rapidly evolving pandemic, Mutual of Omaha has been continuously evaluating our underwriting and new business practices to support business continuity, deliver a consistently high level of service, and maintain our financial strength.

As a result, effective Thursday, April 16, 2020, we are implementing a temporary change. We will not be accepting LTC applications for individuals age 65 and older. All LTC cases not already approved or issued will be postponed and processed as an incomplete application.

We will continue to prequalify applicants 64 and younger. The prequalification will be good for 60 days. If the health of the client changes or the prequalification is past 60 days, you will need to prequalify the applicant again."

I then confirmed this with FoIB Randy G, who added:

"MOO, TransAmerica, NGL, and Thrivent are not accepting any applications for those over the age of 65.

They say temporarily….

Reason is that individuals over the age of 65 will require a home face to face interview.

The nurses who conduct those interviews don’t have sufficient PPEs to enter homes.

Anyway, that’s the story I got.

The companies will still accept applications for those 64 and under. However, there are restrictions to this as well."

Thanks, Herman and Randy!

Oh, *my* take?

I think it's bullcrap: have none of these carriers ever heard of Skype?

from InsureBlog https://ift.tt/3eAfLt5

via

Friday, 17 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

As we noted the other day, many auto insurance carriers have installed discount/refund programs as a result of the pandemic's stifling effect on driving:

"In general, insurers that represent four out of five auto insurance policies sold in the United States have offered to refund some portion of driver premiums."

But that was just a small sampling. This time, FoIB Bill M tips us to a comprehensive list of many (most?) such programs. For example:

"In general, insurers that represent four out of five auto insurance policies sold in the United States have offered to refund some portion of driver premiums."

But that was just a small sampling. This time, FoIB Bill M tips us to a comprehensive list of many (most?) such programs. For example:

■ Amica: 20% credit on April and May premiums

■ The Hartford: 15% refund on April and May premiums (but only for policies in effect as of April 1)

■ Mercury Insurance: 15% credit on April and May premiums

And of course many others. Do click on over to see what your carrier's offering.

from InsureBlog https://ift.tt/3eysvR4

via

Wednesday, 15 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Is it OK to have an HSA plus Medicare? Can I still make contributions once I enroll in Medicare? How about my younger spouse? What else do I need to know?

When you enroll in Medicare Part A or B, you can no longer contribute to your Health Savings Account. When your Medicare begins, your account administrator should change your contribution to your HSA to zero. If you have a spouse who also has an HSA, money can be deposited for him or her. A Health Savings Account is a bank account, not insurance. HSA's have a single owner. Joint ownership is not an option.

You may continue to withdraw money from your HSA after you enroll in Medicare to help pay for medical expenses, such as deductibles, (some) premiums, copayments, and coinsurances. If you use the account for qualified medical expenses, its funds will continue to be tax-free.

If you sign up for Part A after turning 65, Medicare will automatically backdate your Part A effective date by up to 6 months. If you enroll in July, your Part A will be effective January 1 of that year but not before your 65th birthday.

from InsureBlog https://ift.tt/2VpwtSY

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

One of the side effects of the forced shut-down is that folks are driving less - a lot less. And this, in turn, has given auto insurers a good reason to refund at least some of our premiums (less driving = fewer accidents). As we've noted previously, some carriers have been pretty good about this:

"Allstate and American Family Insurance have begun discounting car insurance premiums since many drivers aren’t using their cars as much due to stay-at-home policies aimed at slowing the spread of the coronavirus."

But they're not the only ones and, in fact, some are even better about how they're handling this opportunity. FoIB (and P&C Guru) Bill M tips us to this list of the 10 Best such:

"In general, insurers that represent four out of five auto insurance policies sold in the United States have offered to refund some portion of driver premiums."

Nice!

Leading off in the #10 spot is MapFre, a carrier I've only recently heard of (our eldest is insured with, and speaks very highly of, them). I definitely recommend clicking through to see if your carrier is listed (and in what spot).

"Allstate and American Family Insurance have begun discounting car insurance premiums since many drivers aren’t using their cars as much due to stay-at-home policies aimed at slowing the spread of the coronavirus."

But they're not the only ones and, in fact, some are even better about how they're handling this opportunity. FoIB (and P&C Guru) Bill M tips us to this list of the 10 Best such:

"In general, insurers that represent four out of five auto insurance policies sold in the United States have offered to refund some portion of driver premiums."

Nice!

Leading off in the #10 spot is MapFre, a carrier I've only recently heard of (our eldest is insured with, and speaks very highly of, them). I definitely recommend clicking through to see if your carrier is listed (and in what spot).

from InsureBlog https://ift.tt/2XELjrE

via

Tuesday, 14 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

We've written before about the evolution of coverage for Uber and Lyft drivers, but of course they're not the only ones active in the so-called 'gig-economy.' With social distancing a (hopefully temporary) way of life, more and more folks are turning to services like InstaCart to traverse the various aisles and endcaps, searching for wild game (or cans of soup and maybe a roll of TP or 6). What a lot of folks (myself included!) probably didn't know is that these folks rely on their own transportation to ferry their customer's merch their doorways.

One of our regular readers emails us me about the disturbing truth:

"I want to do some work for Instacart. They do not offer a master insurance policy the way Uber does, you have to provide your own coverage. I have two vehicles, one is covered by a commercial policy, the other is under a regular auto policy.

For the former, commercial coverage is written to cover one type of work, so I can't operate outside of that, thus I have no coverage for Instacart.

For the latter, my broker told me that many insurance companies covering personal vehicles are extending coverage for gigs such as Instacart, but not mine.

My broker pretty much told me that I would have to buy a new commercial policy if I want to do Instacart. I probably won't. And can you imagine how probably 100% of people doing Instacart don't have proper coverage, if any?"

Thank you!!

One of our regular readers emails us me about the disturbing truth:

"I want to do some work for Instacart. They do not offer a master insurance policy the way Uber does, you have to provide your own coverage. I have two vehicles, one is covered by a commercial policy, the other is under a regular auto policy.

For the former, commercial coverage is written to cover one type of work, so I can't operate outside of that, thus I have no coverage for Instacart.

For the latter, my broker told me that many insurance companies covering personal vehicles are extending coverage for gigs such as Instacart, but not mine.

My broker pretty much told me that I would have to buy a new commercial policy if I want to do Instacart. I probably won't. And can you imagine how probably 100% of people doing Instacart don't have proper coverage, if any?"

Thank you!!

from InsureBlog https://ift.tt/3beLMoA

via

Saturday, 11 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Easter means many things to different people, and to some it has no meaning at all.

The colloquial view is bunnies, colored eggs, baskets, new "Sunday" outfits and of course, shiny new shoes. Patent leather if you are a girl.

Just as Passover (Pesach) is a tradition with deep meaning for observant Jews, Easter (Pascha in Greek) is significant to Christians.

Both Passover and Easter are 8 day celebrations excluding Lent which starts 40 days before Easter.

This year Passover and Easter holidays overlap for the first time since 2012.

Perhaps it is more than just a coincidence.

from InsureBlog https://ift.tt/2RtT93y

via

The colloquial view is bunnies, colored eggs, baskets, new "Sunday" outfits and of course, shiny new shoes. Patent leather if you are a girl.

Just as Passover (Pesach) is a tradition with deep meaning for observant Jews, Easter (Pascha in Greek) is significant to Christians.

Both Passover and Easter are 8 day celebrations excluding Lent which starts 40 days before Easter.

This year Passover and Easter holidays overlap for the first time since 2012.

Perhaps it is more than just a coincidence.

from InsureBlog https://ift.tt/2RtT93y

via

Friday, 10 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Wednesday, 8 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

The archetypical celebration of freedom and redemption, Passover, begins this evening.

Because of the pandemic, we have been forced to cancel our traditional - and highly anticipated - seders this year. But we can still enjoy this musical interlude from the Israeli Philharmonic:

חג פסח שמח

from InsureBlog https://ift.tt/2y1Sy1W

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

We spend a lot of time dunking on insurance companies for boneheaded, sometimes egregious behavior.

So it's nice to also point out examples of good corporate behavior, as well. Like the folks at Companion Life:

[click to embiggen]

And they're not the only carrier behaving well. Our friends at OneAmerica Life have announced their CV-19 lapsed policy stance:

"If a life insurance policy lapsed AFTER the policyowner’s resident state issued a moratorium on lapses, then:

1. OneAmerica is automatically extending coverage on these impacted life insurance policies until June 1, 2020.

2. No action is required by you or the policyowner. It is automatic."

Nicely done!

But wait - There's more!

"Allstate and American Family Insurance have begun discounting car insurance premiums since many drivers aren’t using their cars as much due to stay-at-home policies aimed at slowing the spread of the coronavirus."

It's important to note that this is entirely voluntary on the carriers' part, with Allstate estimating their contribution at $600 million, and AmFam's at about a third of that.

But wait - There's more!

"Allstate and American Family Insurance have begun discounting car insurance premiums since many drivers aren’t using their cars as much due to stay-at-home policies aimed at slowing the spread of the coronavirus."

It's important to note that this is entirely voluntary on the carriers' part, with Allstate estimating their contribution at $600 million, and AmFam's at about a third of that.

And please let us know about how other carriers are stepping up - Thanks!

from InsureBlog https://ift.tt/2Ro5XZ7

via

Tuesday, 7 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

This:

December: Do you want health insurance?— Greg Fann (@greg_fann) April 7, 2020

29 million people: No

April: The government will cover COVID-19 costs if you remain uninsured, & other services you would use insurance for will be considered 'elective' and will be postponed. Do you want health insurance?#ACA #Obamacare

from InsureBlog https://ift.tt/2JOzZ48

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

I know, I know, another Business Interruption post - enough, enough!

Except, well, not really:

To recap, Business Interruption coverage is supposed to help reimbursed lost revenue due to a covered, physical loss (such as a fire, or a flood, etc). The issue at hand is whether or not a business forced to close because of the current pandemic is entitled to such reimbursement, since the physical structure remains intact (and distinct from a claim arising from actual contamination). As we've previously mentioned, the answer would presumably be 'No,' but that has since morphed to 'potentially Maybe.'[LINK2]

/sigh

So there's been a loud hue and cry from affected businesses that are facing significant cash flow (as in, zero or very little) problems because they've been forced to close (or drastically pull back). And of course there's increasing pressure on The Powers That Be© to "do something."

But is this wise, let alone appropriate? What should the government's role in this conundrum be (if any)?

Well, let's set the Wayback Machine to almost eleven years ago:[LINK3]

"It’s still far from the norm, but governments around the world are becoming increasingly involved in providing terrorism reinsurance. In addition to catastrophe cover, some are addressing business interruption ... Government involvement has become necessary ... as private insurers and reinsurers would otherwise step back from these risks – either by reducing their exposure or eliminating it completely."

Please note that last: "eliminating it completely."

But is that what really happened?

Well, as our friend and P&C Guru Bill M tips us, pretty much:

"[M]ost companies will probably find it difficult to get an insurance payout because of policy changes made after the 2002-2003 SARS outbreak ... led to millions of dollars in business-interruption insurance claims ... As a result, many insurers added exclusions to standard commercial policies for losses caused by viruses or bacteria."

With the (predictable) result that carriers have what appears to be a bullet-proof claims-denial capability.

So, as with the airline and travel industries (among others), there's a concerted, vocal effort for government intervention:

"[P]roperty and casualty insurance companies are facing growing pressure to tap the industry’s $822 billion in cash reserves.

Lawmakers in New Jersey, Massachusetts and Ohio are considering forcing retroactive policy changes to cover coronavirus business-interruption claims."

Counter-balanced against that, of course, is the (inconvenient?) fact that such coverage was never underwritten, and for which no premium has ever been paid.

#WhatCouldGoWrong?

But is this actually necessary? That is, what if there already existed a policy to cover these circumstances? Surely these would sell like corndogs at the state fair, right?

"Pandemic business insurance — complete with virus coverage — is offered by the broker Marsh."

Oh, that's great! So problem solved, right?

Turns out, not so much:

"It launched its outbreak insurance in 2018.

A few companies in the hospitality and gaming industries showed interest.

But not a single policy was sold."

So, given that, is there some role for government here?

One more trip in the WMB:

"[T]he Terrorism Risk Insurance Act of 2002 to create a “temporary” federal backstop against catastrophic losses. This program subsidized private risk with public funds through a cost-sharing program for which the government does not receive any compensation."

So, government as BI backstop may yet be "a thing."

Guess we'll just have to wait and see.

Except, well, not really:

To recap, Business Interruption coverage is supposed to help reimbursed lost revenue due to a covered, physical loss (such as a fire, or a flood, etc). The issue at hand is whether or not a business forced to close because of the current pandemic is entitled to such reimbursement, since the physical structure remains intact (and distinct from a claim arising from actual contamination). As we've previously mentioned, the answer would presumably be 'No,' but that has since morphed to 'potentially Maybe.'[LINK2]

/sigh

So there's been a loud hue and cry from affected businesses that are facing significant cash flow (as in, zero or very little) problems because they've been forced to close (or drastically pull back). And of course there's increasing pressure on The Powers That Be© to "do something."

But is this wise, let alone appropriate? What should the government's role in this conundrum be (if any)?

Well, let's set the Wayback Machine to almost eleven years ago:[LINK3]

"It’s still far from the norm, but governments around the world are becoming increasingly involved in providing terrorism reinsurance. In addition to catastrophe cover, some are addressing business interruption ... Government involvement has become necessary ... as private insurers and reinsurers would otherwise step back from these risks – either by reducing their exposure or eliminating it completely."

Please note that last: "eliminating it completely."

But is that what really happened?

Well, as our friend and P&C Guru Bill M tips us, pretty much:

"[M]ost companies will probably find it difficult to get an insurance payout because of policy changes made after the 2002-2003 SARS outbreak ... led to millions of dollars in business-interruption insurance claims ... As a result, many insurers added exclusions to standard commercial policies for losses caused by viruses or bacteria."

With the (predictable) result that carriers have what appears to be a bullet-proof claims-denial capability.

So, as with the airline and travel industries (among others), there's a concerted, vocal effort for government intervention:

"[P]roperty and casualty insurance companies are facing growing pressure to tap the industry’s $822 billion in cash reserves.

Lawmakers in New Jersey, Massachusetts and Ohio are considering forcing retroactive policy changes to cover coronavirus business-interruption claims."

Counter-balanced against that, of course, is the (inconvenient?) fact that such coverage was never underwritten, and for which no premium has ever been paid.

#WhatCouldGoWrong?

But is this actually necessary? That is, what if there already existed a policy to cover these circumstances? Surely these would sell like corndogs at the state fair, right?

"Pandemic business insurance — complete with virus coverage — is offered by the broker Marsh."

Oh, that's great! So problem solved, right?

Turns out, not so much:

"It launched its outbreak insurance in 2018.

A few companies in the hospitality and gaming industries showed interest.

But not a single policy was sold."

So, given that, is there some role for government here?

One more trip in the WMB:

"[T]he Terrorism Risk Insurance Act of 2002 to create a “temporary” federal backstop against catastrophic losses. This program subsidized private risk with public funds through a cost-sharing program for which the government does not receive any compensation."

So, government as BI backstop may yet be "a thing."

Guess we'll just have to wait and see.

from InsureBlog https://ift.tt/34j5PPI

via

Monday, 6 April 2020

Saturday, 4 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Medicare supplement plan G 2020. Learn about Medigap G plan.

You don't have to be terminal to run up a lot of medical bills.

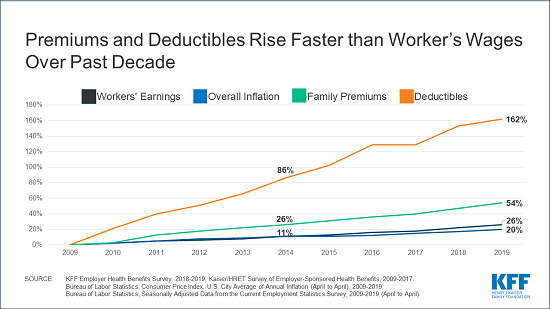

People with diagnosed diabetes incur average medical expenditures of $16,752 per year, of which about $9,601 is attributed to diabetes. On average, people with diagnosed diabetes have medical expenditures approximately 2.3 times higher than what expenditures would be in the absence of diabetes. In the US over 34 million have diabetes.

https://ift.tt/39pghGm

An estimated 22 million people in the US have CVD (Cardio-Vascular Disease). The annual direct cost of care per person is $18,953; for related care the total is $39,036.

https://ift.tt/2V5IT2g

This chart shows annual cost of cancer care for those 65 and over.

https://ift.tt/1Qx8hlV

Limit your out of pocket costs with Medicare supplement plan G.

from InsureBlog https://ift.tt/2V3SFSy

via

You don't have to be terminal to run up a lot of medical bills.

People with diagnosed diabetes incur average medical expenditures of $16,752 per year, of which about $9,601 is attributed to diabetes. On average, people with diagnosed diabetes have medical expenditures approximately 2.3 times higher than what expenditures would be in the absence of diabetes. In the US over 34 million have diabetes.

https://ift.tt/39pghGm

An estimated 22 million people in the US have CVD (Cardio-Vascular Disease). The annual direct cost of care per person is $18,953; for related care the total is $39,036.

https://ift.tt/2V5IT2g

This chart shows annual cost of cancer care for those 65 and over.

https://ift.tt/1Qx8hlV

Limit your out of pocket costs with Medicare supplement plan G.

from InsureBlog https://ift.tt/2V3SFSy

via

Friday, 3 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

News flash: ACA exchanges are open and all states have Special Enrollment Periods!

News flash: ACA exchanges are open and all states have Special Enrollment Periods!In a day and age when 240 characters is our limit for reading news, it becomes very important that we don't overlook the facts within the story. Unfortunately our media outlets would rather garner clicks and scare people than provide a real understanding of what people can do.

Look at these headlines:

Trump Rejects Obamacare Special Enrollment Period Amid Pandemic - Politico

Trump Rejects Opening Obamacare Enrollment for Uninsured Americans - Fox Business News

Obamacare Markets Will Not Reopen, Trump Decides - New York Times

The list goes on: The Daily Beast, Salon, Business Insider, NBC, all have headlines that create fear.

This shameful tactic is bad enough during normal times, but playing on people's emotions during a pandemic where many are losing their jobs and their benefits is downright f'ed up.

Instead of dwelling on a lost cause, I would like to share the facts. Not only the facts as it relates to Special Enrollment Periods (SEP) being available, but also the challenges an individual faces when signing up for coverage.

An SEP is an enrollment opportunity for individuals dealing with certain life events including losing health coverage, moving, getting married, having a baby, or adopting a child. Aside from an SEP, someone may also qualify for COBRA (likely high cost) or Medicaid/CHIP (income limits apply).

For now we will focus on losing health coverage.

When you lose your job you have 60 days before or 60 days following the event to enroll in a plan. To enroll you need to create an account at Healthcare.gov (or your state's exchange platform). When creating an account you are asked quite a bit about your demographics. Answering these questions are essential to your account and don't require much heavy lifting to complete.

The more challenging parts of the application process deal with providing your projected income, understanding your results, and uploading the proper documents to finalize your insurance.

During the application process you will be asked to provide your projected income for the year. This is the first challenge as nobody knows how much they will make in the future. It's important to note that many sources of income count including wages, tips, income from investments/rentals, Social Security, retirement/pensions, and unemployment. I highlight the last because it will likely be a focus for those losing employer based insurance.

Once you have completed the basic sections you will be able to "review your results". It is here where you find out if you qualify for a subsidy or not. Also in this document will be details on what you need to provide as proof you are losing insurance coverage. This document - once you receive it - will have to be uploaded and sent to healthcare.gov. Documents that can be submitted include a letter from the health insurance company, a letter from your employer, a letter regarding COBRA, or many others based on your situation.

From here you will determine how much of your subsidy you want to use on a monthly basis (we recommend all of it), review all plans and prices, make a plan selection, and then pay your initial premium.

It's important to remember that if you have already lost insurance that you must pick a plan within 60 days of losing coverage, submit documents within 30 days of picking a plan, and your new plan won't start until the first of the month after you have picked a plan.

This is a very cumbersome process for most and there are many pitfalls that come along with trying to navigate the website on your own. Above everything I would recommend finding a licensed agent in your area to help you through the process. In many areas there is no cost for this assistance as compensation is built in to the insurance premiums you pay.

One last note, if you are looking for insurance make sure you complete the process within the required timeframe. Failing to do so will result in you having to wait until open enrollment which doesn't start your coverage until January 1, 2021.

from InsureBlog https://ift.tt/39FmMFh

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Not all heroes wear capes.

Or even clothes, for that matter:

Or even clothes, for that matter:

"The British company MedFet, which describes itself as the "only online store 100% dedicated to medical fetish, kink, and roleplay," donated medical scrubs to a hospital to help its staff protect themselves from the virus while treating an influx of patients."

Here in the states, we're seeing company's like MyPillow making masks, and GM building ventilators, so this is definitely a bit ... er ... different.

Still, it speaks to the fallacy that nationalized, single-payer healthy "care" schemes are somehow better up to the daunting task than our admittedly flawed system.

#Medicaid4AllFail

from InsureBlog https://ift.tt/3dQaygn

via

Thursday, 2 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

New guy on the block:

Looking for health insurance outside of Open Enrollment? @Decent's Chief Health Plan Officer @Molly23Moore explains your options. If you're self-employed in Austin, we have the only comprehensive plans for sale year round at https://t.co/8eZ1l17obM. Either way, we can help. pic.twitter.com/mPbsnyYhgl— Nick Soman (@nicksoman) April 1, 2020

On the surface, it's a (now) standard MEWA/AHP for self-employed Lone Star Staters, but also a hybrid of insurance & DPC.

The FAQ says doesn't price for pre-ex, which is nice, as well.

I reached out to their CEO, who assured me that:

"It’s not underwritten at all. We ask your age, your zip code, and whether you smoke. Our plans cover comprehensive EHBs too. You need to be self-employed to sign up"

And there's this: the versions of this that are available in my market require membership in an association or chamber of commerce, which can add substantially to the actual cost (one such runs $1,000/year in chamber fees!). Decent's differtent:

"You become part of the Texas Freelance Association, which is free to join, when you choose one of our plans."

Nice!

And I also like that they do use agents/brokers for marketing.

I do have some concerns about the product labeling, but not a huge deal.

Will be interesting to see if this catches on.

from InsureBlog https://ift.tt/2UDDHUc

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Maybe, maybe not:

Earlier this week, we pondered how (and/or if) off-label uses of certain meds might be covered. I reached out to one of our carriers (whose rep was willing to at least kick this up the food chain for me). In the meantime, a commenter points out:

"The FDA issued an emergency-use authorization late Sunday for chloroquine and its next-generation version, hydroxychloroquine, as treatments for the novel coronavirus"

So it will be interesting to see how that plays out.

Oh, I have now heard back from my "inside source," who offers this helpful perspective on the general subject:

Earlier this week, we pondered how (and/or if) off-label uses of certain meds might be covered. I reached out to one of our carriers (whose rep was willing to at least kick this up the food chain for me). In the meantime, a commenter points out:

"The FDA issued an emergency-use authorization late Sunday for chloroquine and its next-generation version, hydroxychloroquine, as treatments for the novel coronavirus"

So it will be interesting to see how that plays out.

Oh, I have now heard back from my "inside source," who offers this helpful perspective on the general subject:

"Once a physician writes a prescription and the member has it filled by a pharmacy, the pharmacist won’t know specifically what is the patient’s diagnosis, or whether or not the physician prescribed something for the patient that is prescribed for an off label use.

Many specific drugs have programs such as Prior Approval and Step Therapy associated with them. The latter will require the physician to submit to Anthem for a prior authorization, indicating why a member needs a specific medication - or in the case of Step Therapy, the patient would have to try a medication in that same class, before what is written can be filled. The latter typically halts the use of “off label” prescribing for most of the higher cost brand medications."

Thank you!

from InsureBlog https://ift.tt/2R4rcPw

via

Wednesday, 1 April 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

No, not at all, but a conversion opportunity nonetheless.

Many folks choose term life products as a biggest-bang-for-the-buck life insurance option. These plans feature lower premiums than their permanent coverage brethren (eg Whole and Universal, etc), and the premiums are guaranteed for a specific number of years, after which the rates tend to sky-rocket. By then, of course, many (most?) folks no longer need all that coverage, and at least a few who do need it no longer qualify health-wise for a new plan.

What to do?

Well, one really helpful feature of most term life plans is their convertibility feature, which allows one to purchase a like amount (or less, if desired) of permanent insurance with rates that are guaranteed for the rest of one's day's on this mortal coil. Yes, they can be a bit pricey, as well, but there are some unique benefits, as described by FoIB Brian D:

"So, what can you do when you realize you need all or a portion of your life insurance to last beyond the initial length of your term?It means that any time after the first policy year, you can change from a limited-time benefit to a permanent one without answering health questions, having bloodwork or any other physical examination. In most cases, the death benefit for the new permanent policy will be in force until age 121, providing you with lifelong coverage."

Highly recommended reading (no foolin'!).

Many folks choose term life products as a biggest-bang-for-the-buck life insurance option. These plans feature lower premiums than their permanent coverage brethren (eg Whole and Universal, etc), and the premiums are guaranteed for a specific number of years, after which the rates tend to sky-rocket. By then, of course, many (most?) folks no longer need all that coverage, and at least a few who do need it no longer qualify health-wise for a new plan.

What to do?

Well, one really helpful feature of most term life plans is their convertibility feature, which allows one to purchase a like amount (or less, if desired) of permanent insurance with rates that are guaranteed for the rest of one's day's on this mortal coil. Yes, they can be a bit pricey, as well, but there are some unique benefits, as described by FoIB Brian D:

"So, what can you do when you realize you need all or a portion of your life insurance to last beyond the initial length of your term?It means that any time after the first policy year, you can change from a limited-time benefit to a permanent one without answering health questions, having bloodwork or any other physical examination. In most cases, the death benefit for the new permanent policy will be in force until age 121, providing you with lifelong coverage."

Highly recommended reading (no foolin'!).

from InsureBlog https://ift.tt/3aAbZ09

via

Tuesday, 31 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

This is HUGE - Humana waiving all CV-19 costs, treatment included:

"[C]osts related to subsequent treatment for COVID-19—including inpatient hospital admissions— will be waived for enrollees of Medicare Advantage plans, fully insured commercial members, Medicare Supplement and Medicaid.The waiver applies to all medical costs related to the treatment of COVID-19 as well as FDA-approved medications or vaccines when they become available."

from InsureBlog https://ift.tt/2w39Gnr

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Well, off-label, actually:

I've been asked how carriers might handle the off-label use of meds like Chloroquine (generally used as an anti-malarial drug, and also for lupus) . That is, would this "off-label use" still be considered a valid/covered expense?

To that end, I've reached out to one of our carriers (and been trying to do so with others) to see how this issue has historically been addressed. By way of example, I've posed this:

I've been asked how carriers might handle the off-label use of meds like Chloroquine (generally used as an anti-malarial drug, and also for lupus) . That is, would this "off-label use" still be considered a valid/covered expense?

To that end, I've reached out to one of our carriers (and been trying to do so with others) to see how this issue has historically been addressed. By way of example, I've posed this:

"Researching a post on how carriers *might* handle use of chloroquine for COVID-19. NOT asking how y'all will handle that issue specifically, but just how/if cover off-label use of meds for medically-necessary issues. For example, using Colchicine (gout med) for Pericarditis (pericardium inflammation). *In general*, is this kind of thing usually covered?"As one might imagine, carriers are (understandably) reluctant to pre-adjudicate a hypothetical claim, and so I've been very carefiul to emphasize that I'm looking only for a historical perspective, which may be of value in the current situation.

So far, I've been kicked up the food chain, but still awaiting an on-point response.

If you are in a position (or know someone who is) to help us with an answer, I would be very grateful for your help. And, of course, confidentiality is a given.

from InsureBlog https://ift.tt/2JtHJZ3

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

From our friends at the Ohio Insurance Agents association:

"Phishing emails are a great way for hackers to gain access to your system. Phishing is a cyber-crime term that describes how criminals pose as legitimate institutions or a trustworthy entity/individual to trick you into providing sensitive data such as login ID’s and passwords.

Due to the COVID-19 outbreak, cyber-criminals are using fear and uncertainty to prompt people to click on emails that promise supplies of paper products, hand sanitizer, and other products that are in short supply. Some reports are indicating that consumers are giving credit card information thinking they are buying supplies for their household. Phishing doesn’t come in just the form of emails; you need to be aware that phishing can happen via text and phone calls as well."

So what can you do?

Well, for one thing, always check the return address on these emails, they'll often (usually?) be an obvious fake. And before clicking any links, check with your (or your company's) IT folks for verification.

Be careful out there!!

"Phishing emails are a great way for hackers to gain access to your system. Phishing is a cyber-crime term that describes how criminals pose as legitimate institutions or a trustworthy entity/individual to trick you into providing sensitive data such as login ID’s and passwords.

Due to the COVID-19 outbreak, cyber-criminals are using fear and uncertainty to prompt people to click on emails that promise supplies of paper products, hand sanitizer, and other products that are in short supply. Some reports are indicating that consumers are giving credit card information thinking they are buying supplies for their household. Phishing doesn’t come in just the form of emails; you need to be aware that phishing can happen via text and phone calls as well."

So what can you do?

Well, for one thing, always check the return address on these emails, they'll often (usually?) be an obvious fake. And before clicking any links, check with your (or your company's) IT folks for verification.

Be careful out there!!

from InsureBlog https://ift.tt/2QTV0OP

via

Monday, 30 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

A few days ago, we mentioned that (at least) one of our carriers was offering to "adjust the customer’s current bill and to waive any late fees for any premium payments due between March 16 and April 30."

Well that was then, and this is now, and it's no longer just a nice gesture on the carriers' part. Our friends at the Ohio Insurance Agents association just tipped us:

Well that was then, and this is now, and it's no longer just a nice gesture on the carriers' part. Our friends at the Ohio Insurance Agents association just tipped us:

"This bulletin pertains to all insurers (“Insurers”) providing property and casualty, life, and long term care insurance policies (“policies”) in the State of Ohio. The purpose of this bulletin is to notify Insurers that they must provide their insureds with at least a 60-day grace period to pay insurance premiums or submit information."

As with the similar decree about group insurance (and from the Feds on ObamaPlans), it's critical to keep in mind that this is a deferral, not a waiver: at some point the bill will come due. So think long and hard about your financial status now vs early summer.

from InsureBlog https://ift.tt/2Us3m2k

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Got this from our primary P&C carrier:

"Employers must report COVID-19 illness in workplace."

Which makes sense, but (as I pointed out at that post) seems to contradict HIPAA/privacy requirements, as well as guidance we noted the other day:

"Employers must report COVID-19 illness in workplace."

Which makes sense, but (as I pointed out at that post) seems to contradict HIPAA/privacy requirements, as well as guidance we noted the other day:

"Applicable law limits Anthem’s ability to share an individual’s protected health information with an employer absent an authorization or certain extenuating circumstances. As a result, Anthem is limited by law in its ability to disclose individual’s protected health information to an employer."

So how to square that circle?

from InsureBlog https://ift.tt/2wNdHwK

via

Friday, 27 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

This is what I love (and hate) about the insurance biz: to paraphrase a former POTUS, it depends on what the meaning of "covered loss" is.

Hunh?

Well, last week we posted what we thought was the definitive answer to the question of whether one's Business Interruption coverage would be triggered by the current Pandemic:

"In the event of my absence, if anyone for commercial lines calls and asks if there is any business income coverage due to their business shutting down during the Coronavirus outbreak, the answer is "No"."

And that, it seemed (at the time, at least) was that.

But maybe not:

That is, maybe BI cover does extend, even absent a "direct, physical loss."

The article notes, for example that if "a property has been contaminated by an infected person, or because COVID-19 is in the airspace or on surfaces, this will likely constitute direct physical damage." I would argue that this alone doesn't seem to reach the threshold, but then, I'm not the judge or the claims adjustor.

And, of course, that particular cite pertained to a New Jersey Appellate Court decision, so its relevance in other jurisdictions is up for grabs.

And there's this:

"Depending on the circumstances, the governing law, and the applicable policy’s language, they may very well be wrong. By way of example, some policies require “direct physical loss of or damage to” property. “Loss” and “damage” are not synonymous and may require separate analysis."

Will be interesting to see how this shakes out.

As always, consult with your own agent about how your policy may (or may not) handle this.

Hunh?

Well, last week we posted what we thought was the definitive answer to the question of whether one's Business Interruption coverage would be triggered by the current Pandemic:

"In the event of my absence, if anyone for commercial lines calls and asks if there is any business income coverage due to their business shutting down during the Coronavirus outbreak, the answer is "No"."

And that, it seemed (at the time, at least) was that.

But maybe not:

"By way of example, some policies require “direct physical loss of or damage to” property. “Loss” and “damage” are not synonymous and may require separate analysis. Such wording could arguably trigger coverage where there is a loss of the premise’s use (even if the property is not physically damaged)."

That is, maybe BI cover does extend, even absent a "direct, physical loss."

The article notes, for example that if "a property has been contaminated by an infected person, or because COVID-19 is in the airspace or on surfaces, this will likely constitute direct physical damage." I would argue that this alone doesn't seem to reach the threshold, but then, I'm not the judge or the claims adjustor.

And, of course, that particular cite pertained to a New Jersey Appellate Court decision, so its relevance in other jurisdictions is up for grabs.

And there's this:

"Depending on the circumstances, the governing law, and the applicable policy’s language, they may very well be wrong. By way of example, some policies require “direct physical loss of or damage to” property. “Loss” and “damage” are not synonymous and may require separate analysis."

Will be interesting to see how this shakes out.

As always, consult with your own agent about how your policy may (or may not) handle this.

from InsureBlog https://ift.tt/2xt9jmF

via

Thursday, 26 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

That is, premium deferment options similar to what we're seeing in the group market:

The key is that the Feds seem to be allowing such flexibility, not requiring it. And, as we've noted with the group extended grace period offer, these premiums are *deferred*, not waived; that is, the piper will eventually have to be paid.

Be careful...

Full text of notice here.

Updates shortly.

(CMS) posted Payment &; Grace Period Flexibilities Issuers Offering Coverage FFM & SBE, CMS will exercise enforcement discretion to permit issuers lans (QHPs) & (SADPs) to extend payment deadlines for initial payments as well as ongoing premiums during the period of the COVID-19— HAFA (@TheNolanGroup) March 25, 2020

The key is that the Feds seem to be allowing such flexibility, not requiring it. And, as we've noted with the group extended grace period offer, these premiums are *deferred*, not waived; that is, the piper will eventually have to be paid.

Be careful...

Full text of notice here.

Updates shortly.

from InsureBlog https://ift.tt/39lxdO6

via

Wednesday, 25 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Courtesy of co-blogger Mike:

During a visit to my doctor, I asked him, "How do you determine whether or not an older person is ready to make a Long Term Care claim for Assisted Living?"

"Well," he said, "we fill up a bathtub, then we offer a teaspoon, a teacup and a bucket to the person to empty the bathtub."

"Oh, I understand," I said. "A normal person would use the bucket because it is bigger than the spoon or the teacup."

"No" he said. "A normal person would pull the plug. Here’s your claim form."

During a visit to my doctor, I asked him, "How do you determine whether or not an older person is ready to make a Long Term Care claim for Assisted Living?"

"Well," he said, "we fill up a bathtub, then we offer a teaspoon, a teacup and a bucket to the person to empty the bathtub."

"Oh, I understand," I said. "A normal person would use the bucket because it is bigger than the spoon or the teacup."

"No" he said. "A normal person would pull the plug. Here’s your claim form."

from InsureBlog https://ift.tt/33LU6cv

via

Tuesday, 24 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Planning to retire? You are Medicare age but your spouse is not. What are your options?

You MAY continue to work if that is available.

You can enroll with Medicare, your spouse opts for an #Obamacare plan.

Or you take Medicare and spouse chooses COBRA.

Just don't pick COBRA for BOTH of you. That triggers the Medicare COBRA trap.

#Medicare #YoungerSpouse #COBRA

from InsureBlog https://ift.tt/2QHyZm1

via

|

| Age 65 Younger Spouse |

You MAY continue to work if that is available.

You can enroll with Medicare, your spouse opts for an #Obamacare plan.

Or you take Medicare and spouse chooses COBRA.

Just don't pick COBRA for BOTH of you. That triggers the Medicare COBRA trap.

#Medicare #YoungerSpouse #COBRA

from InsureBlog https://ift.tt/2QHyZm1

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

I think we've had more P&C-related posts the past week or so than the past year combined. But it is Insureblog, so...

1 - From Cincinnati Insurance Company (and, I'm sure, we'll see other carriers following suit):

1 - From Cincinnati Insurance Company (and, I'm sure, we'll see other carriers following suit):

"Billing

Policyholders are understandably concerned about their ability to pay premiums as government mandated closures continue to increase. To help, we’re suspending all property casualty cancellations due to nonpayment from March 16 to April 30 – or later if required by an individual state.

While we hope that most policyholders can stick with their current payment arrangements, if you have a standard lines commercial, personal or life policyholder asking about alternative payment arrangements our billing associates are authorized to adjust the customer’s current bill and to waive any late fees for any premium payments due between March 16 and April 30. This is not a waiver of payments during the suspension period, but an extension or grace period for those directly impacted by this pandemic. Please have them contact our billing departments"

2 - We've discussed Special Event coverage before:

"World Furniture Mall "promised that if the Bears shut out the Packers in the season opener at Lambeau Field in Green Bay, Labor Day weekend shoppers would get their furniture free."

And of course there's so-called 'Hole-in-one' cover and the like, as well.

Typically, these cover unforeseen issues like weather or the like, but what about the current situation? Well, our friends at the Ohio Insurance Agents association offer this heads' up:

"Read the policy language. Every policy is different. Prepare yourself by reading the policy language and specific exclusions on the Special Event Policies that you have issued. In addition, contact your underwriters for clarification on the exclusions to ensure you have a thorough understanding and will be able to communicate it back to your clients."

Always good advice.

from InsureBlog https://ift.tt/2Uw15C8

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Let's say that you deliberately skipped Open Enrollment (because, hey, why not?). And let's say that you now regret that decision.

No problem, mi amigo:

"Eleven States Now Letting Uninsured Sign Up for Obamacare"

Never let a crisis go to waste.

#Medicaid4All

[Hat Tip: FoIB Holly R]

No problem, mi amigo:

"Eleven States Now Letting Uninsured Sign Up for Obamacare"

Never let a crisis go to waste.

#Medicaid4All

[Hat Tip: FoIB Holly R]

from InsureBlog https://ift.tt/3dARNNU

via

Monday, 23 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Just off conference call with Anthem execs, lots of interesting info, and will try to put together a more complete post, but some highlights:

■ Extraordinary focus on "Virtual Care" - what we've been calling 'telehealth' or 'telemedicine' and which has been mostly under the radar, until now. This is as much about capacity as it is social distancing, and the government is requiring carrier (like Anthem) to offer these services with no cost-sharing.

■ Relaxed rules on early refills for maintenance meds - this makes sense, again to minimize travel and maximize social distancing.

■ Group Plan Special Enrollment - This was a surprise to me: employees who initially waived group coverage can actually enroll between now and April 3rd, with full coverage.

There's more, and I'll try to update as quickly as possible. Stray tuned.

from InsureBlog https://ift.tt/2UdXAkT

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Last Friday, we posted a breaking news item pertaining to group health insurance plans and grace periods:

"Employers can defer their premium payments for health insurance for up to 2 months."

Now, we have more details:

"Insurers must permit employers to continue covering employees under group policies even if the employee would become ineligible due to a decrease in hours worked ... Employees who lose coverage are eligible for a special enrollment perio to enroll in new [individual] coverage."

More at this link.

One presumes other states will also roll out similar decrees.

Oh!

We also got some interesting info from Anthem, courtesy of FoIB Beth D:

Hadn't even considered the HIPAA/Privacy angles here. Thanks, Anthem (and Beth)!

And one more thing (because I'd been wondering about how this will affect self-insured plans, as well):

So there ya go.

"Employers can defer their premium payments for health insurance for up to 2 months."

Now, we have more details:

"Insurers must permit employers to continue covering employees under group policies even if the employee would become ineligible due to a decrease in hours worked ... Employees who lose coverage are eligible for a special enrollment perio to enroll in new [individual] coverage."

More at this link.

One presumes other states will also roll out similar decrees.

Oh!

We also got some interesting info from Anthem, courtesy of FoIB Beth D:

Q: Can Anthem provide my company with information regarding COVID-19 cases within our member population?

A: Applicable law limits Anthem’s ability to share an individual’s protected health information with an employer absent an authorization or certain extenuating circumstances. As a result, Anthem is limited by law in its ability to disclose individual’s protected health information to an employer.

Q: Can an employer receive information on the number of claims — but not specific names — for COVID-19 tests and related services?

A: No. Currently, it may be possible to identify someone specifically even if, for example, their name is not shared. We recommend checking in with local health authorities to understand the total number of cases in any given area.

Hadn't even considered the HIPAA/Privacy angles here. Thanks, Anthem (and Beth)!

And one more thing (because I'd been wondering about how this will affect self-insured plans, as well):

Self-insured plans no longer have the option not to waive out-of-pocket member expenses for the diagnostic test and the visit associated with the test, as laid out in the federal mandate.

So there ya go.

from InsureBlog https://ift.tt/3dqXNZh

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

We've been discussing some of the insurance issues which agents, companies and clients are facing while the Pandemic continues. Obviously, people still need insurance, and of course a lot of policies are negotiated at the proverbial kitchen table. But what happens when the kitchen table meets 'social distancing?'

Well, our friends at Mutual of Omaha have some suggestions:

"We encourage you to also do your part to slow the spread of the coronavirus. You're likely rethinking how you can keep yourself and others safe in a business that's built on relationships with people and, most often, face-to-face interactions ... We strongly encourage you not to conduct in-person client meetings and we should all be prudent to exercise an abundance of caution."

And they go on to list some reasonable alternatives:

[QUOTE BOX]

o Opt for video meetings or phone calls when possible.

o Avoid in-person meetings if either you or another participant is at risk.

They also suggest contacting folks in advance, and avoid meetings where any of the participants aren't feeling well. And they also suggest - and I think this is particularly helpful - that if one does "proceed with an in-person meeting, please document the client's agreement to meet ... This will be key if there are any questions later regarding meetings or participants."

Or, as our friends at Issue Insurance call it, 'Professional Distancing.'

I like it.

All of these strictures apply, of course, to any insurance sales opportunity, from a simple auto policy renewal to complex Long Term Care insurance reviews.

And remember Sgt Esterhaus' admonition.

Of course, Professional Distancing just got a lot easier for us folks in the Buckeye State.

Well, our friends at Mutual of Omaha have some suggestions:

"We encourage you to also do your part to slow the spread of the coronavirus. You're likely rethinking how you can keep yourself and others safe in a business that's built on relationships with people and, most often, face-to-face interactions ... We strongly encourage you not to conduct in-person client meetings and we should all be prudent to exercise an abundance of caution."

And they go on to list some reasonable alternatives:

[QUOTE BOX]

o Opt for video meetings or phone calls when possible.

o Avoid in-person meetings if either you or another participant is at risk.

They also suggest contacting folks in advance, and avoid meetings where any of the participants aren't feeling well. And they also suggest - and I think this is particularly helpful - that if one does "proceed with an in-person meeting, please document the client's agreement to meet ... This will be key if there are any questions later regarding meetings or participants."

Or, as our friends at Issue Insurance call it, 'Professional Distancing.'

I like it.

All of these strictures apply, of course, to any insurance sales opportunity, from a simple auto policy renewal to complex Long Term Care insurance reviews.

And remember Sgt Esterhaus' admonition.

Of course, Professional Distancing just got a lot easier for us folks in the Buckeye State.

from InsureBlog https://ift.tt/3apapy4

via

Friday, 20 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

Co-blogger Patrick just sent me this:

.@LtGovHusted: @OHInsurance is issuing an order to allow employers to take care of employees with a grace period for insurance premiums. Employers can defer their premium payments for health insurance for up to 2 months.— Governor Mike DeWine (@GovMikeDeWine) March 20, 2020

This is relevant to our post the other day wondering about the short term future of group health plans, and is welcome news indeed.

from InsureBlog https://ift.tt/3a6XkJH

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

While we've been focused primarily on the health insurance aspect of the pandemic, we've also blogged petty extensively about Business Interruption coverage in commercial lines packages, and even noted how the P&C side of the biz is likely sheltered from catastrophic losses.

But something I hadn't seen addressed, at least until now, is the Worker's Comp issue:

That is, as more workers succumb to the Chinese Coronavirus while on the job. I can see this; for example:

But something I hadn't seen addressed, at least until now, is the Worker's Comp issue:

Michel Leonard of @iiiorg says highest impact will be on Work Comp with exposure highest for carriers covering medical, first responders, transportation and retail. Need for greater education around policies and coverages regarding #COVID19— National Association of Insurance Commissioners (@naic) March 20, 2020

That is, as more workers succumb to the Chinese Coronavirus while on the job. I can see this; for example:

Had to meet a relative at the ER yesterday, and while she was squadded in, I had to walk to the ER from the parking lot. I was immediately stopped by a very polite yong nurse tech(?) who took and reported my temp and asked a few health questions. Her PPE consisted of a blanket (it was a bit chilly, and the door was propped open) and a pair of latex gloves. And yet, here I waltz in, breathing (and maybe coughing?) and I'm thinking that that blanket and those gloves are no match for CV-19.

#Food4Thought

#Food4Thought

from InsureBlog https://ift.tt/33Bl7Pq

via

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

The good news is that, through government action and insurance company efforts, (initial) CV-19 testing is "free" (scare quotes because, well, we all know why).

The bad news, as FoIB Sheron Sidbury notes, is less obvious:

And it gets worse: pretty much all individual plans, and not a few group ones, are built on an HMO-chassis, which means if the only or closest) treatment facility is out-of-network, you're outta luck.

Ouch.

The bad news, as FoIB Sheron Sidbury notes, is less obvious:

I wonder how many people think their health insurance will pay for Corvid19 treatments. Waving a copay for the test is not the same as waving a fee for your "treatment". HDHP folks you are still on the hook. They ar only waving copays for the test.https://t.co/XHs7skx0F2— Sheron E Sidbury (@SheronESidbury) March 19, 2020

And it gets worse: pretty much all individual plans, and not a few group ones, are built on an HMO-chassis, which means if the only or closest) treatment facility is out-of-network, you're outta luck.

Ouch.

from InsureBlog https://ift.tt/2xWGaQX

via

Thursday, 19 March 2020

Insurance Tips and trik auto insurance, auto insurance quotes, auto insurance companies, auto insurance florida, auto insurance quotes online, auto insurance america

As we continue to monitor carriers' response to the pandemic, here's some helpful info from our friends at Companion Life (full discourage: CompLife is our go-to carrier for ancillary non-medical group coverage, including short- and long-term disability plans):

"If you have, or have been exposed to, COVID-19 and have been diagnosed by a certified medical professional, you can file a short-term disability claim."

Subject to waiting periods and the like.

Now, we've also been following the Business Interruption coverage issue:

"In the event of my absence, if anyone for commercial lines calls and asks if there is any business income coverage due to their business shutting down during the Coronavirus outbreak, the answer is "No"."

Okay, but what about disability coverage?

Well:

"We understand that some of our groups maybe faced with temporarily closing their doors dure to COVID-19. As an employer, if you choose to deem your employees still "actively emoloyed" and "benefits-eligible" during that temporary closure, Companion Life will recognize those statuses."

This is similar to the Medical Mutual of Ohio stance on group plans.

It's important to note, of course, that as with the BI issue, absent an actual "physical loss" these folks aren't 'disabled,' so aren't eligible for benefits.

On the other hand, and in keeping with current sentiments currently coming out of DC, the company is "extending the grace period for remitting premium payments."

Kudos.

"If you have, or have been exposed to, COVID-19 and have been diagnosed by a certified medical professional, you can file a short-term disability claim."

Subject to waiting periods and the like.

Now, we've also been following the Business Interruption coverage issue:

"In the event of my absence, if anyone for commercial lines calls and asks if there is any business income coverage due to their business shutting down during the Coronavirus outbreak, the answer is "No"."

Okay, but what about disability coverage?

Well:

"We understand that some of our groups maybe faced with temporarily closing their doors dure to COVID-19. As an employer, if you choose to deem your employees still "actively emoloyed" and "benefits-eligible" during that temporary closure, Companion Life will recognize those statuses."

This is similar to the Medical Mutual of Ohio stance on group plans.

It's important to note, of course, that as with the BI issue, absent an actual "physical loss" these folks aren't 'disabled,' so aren't eligible for benefits.

On the other hand, and in keeping with current sentiments currently coming out of DC, the company is "extending the grace period for remitting premium payments."

Kudos.

from InsureBlog https://ift.tt/2U6ZoMx

via

Subscribe to:

Comments (Atom)